🏦 Can a bank really take possession of your property without first obtaining a court order?

Most people assume the answer is no. After all, how can someone lose possession of a property without years of litigation? Yet thousands of borrowers across India discover that banks have powerful recovery rights under a law known as the SARFAESI Act.

Understanding how this law works is important not only for borrowers but also for property owners, guarantors, legal heirs, and lawyers dealing with recovery proceedings.

🏦 SARFAESI Act Explained

Imagine this scenario: You miss a few loan payments. One day, a notice arrives from the bank. A few months later, the bank takes possession of your property, and soon after, the property is listed for auction. Many people are shocked when they discover that all of this can happen without the bank first obtaining a court decree. This is where the SARFAESI Act comes in.

⚖️ What Is the SARFAESI Act?

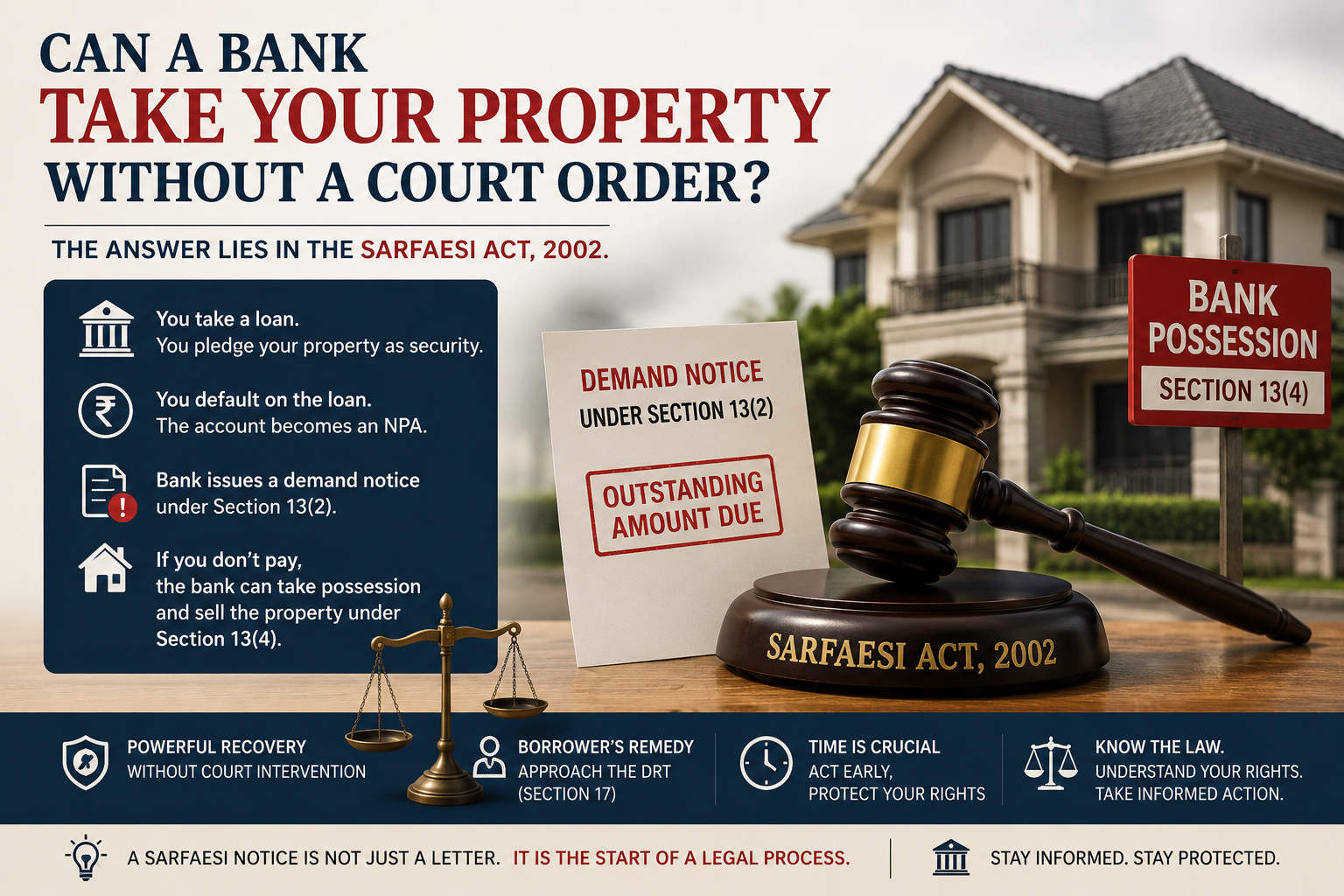

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act) was enacted to help banks and financial institutions recover secured debts more efficiently. Before SARFAESI, lenders often had to spend years in litigation before recovering their dues. The Act changed that by allowing eligible banks and financial institutions to enforce their security interest without first filing a civil suit.

In simple terms, if a loan is secured by property and the borrower defaults, the bank may take steps to recover its dues directly against the secured asset.

📋 How Does the Process Begin?

The SARFAESI process usually starts after the loan account is classified as a Non-Performing Asset (NPA). The bank then issues a:

Section 13(2) Demand Notice

This notice generally gives the borrower 60 days to discharge the outstanding liability. The borrower may:

Ignoring this notice is often a costly mistake.

🏠 What Happens After the 60 Days?

If the dues remain unpaid, the bank may proceed under:

Section 13(4)

The bank may:

This is usually the stage where borrowers realize the seriousness of the proceedings.

🔍 Can the Borrower Challenge the Bank's Action?

Yes. One of the most important safeguards under the Act is the right to approach the Debt Recovery Tribunal (DRT). A borrower or any person aggrieved by measures taken under Section 13(4) may file a:

Securitisation Application (SA)

before the DRT. The Tribunal can examine:

This provides an opportunity for borrowers to contest the bank's actions.

🤔 A Common Misunderstanding

Many people believe that filing a case automatically stops SARFAESI proceedings. That is not always true. The bank's actions do not automatically come to a halt merely because proceedings are pending. Appropriate relief must generally be obtained from the Tribunal. This is why timing is extremely important in SARFAESI matters.

⚖️ Can a Bank Proceed Under SARFAESI While an OA Is Pending Before the DRT?

This is one of the most frequently asked questions. Suppose a bank has already filed an Original Application (OA) before the DRT seeking recovery of debt. Can it still proceed under SARFAESI? In many situations, yes. Courts have repeatedly recognized that remedies under the SARFAESI Act and the RDB Act are generally complementary. A bank may pursue recovery proceedings before the DRT while simultaneously enforcing its security interest under SARFAESI. This often surprises borrowers who assume that one proceeding must end before the other begins.

🚨 Why Property Owners Should Pay Attention

SARFAESI disputes are not limited to borrowers.

Questions frequently arise involving:

- Co-owners

- Legal heirs

- Purchasers

- Tenants

- Third-party claimants

In some cases, the dispute is not about the loan itself but about who actually owns the property.

These situations can become legally complex and often require immediate action.

💡 Practical Lessons

If you receive a SARFAESI notice:

✔️ Do not ignore it

✔️ Verify the outstanding amount

✔️ Check the loan documents

✔️ Understand the timeline

✔️ Seek legal advice at the earliest stage

Delays often reduce available options.

🎯 Final Thoughts

The SARFAESI Act was introduced to speed up debt recovery.

For banks, it is a powerful recovery mechanism.

For borrowers and property owners, it is a reminder that secured assets can be enforced without lengthy court proceedings.

Understanding the process, timelines, and available remedies is often the difference between reacting late and responding effectively.

Because in SARFAESI matters, the most important question is not whether action can be taken.

It is whether you act before it is too late.

💬 Discussion

Here's an interesting question:

Can a bank continue with a property auction under SARFAESI even when an OA for recovery is still pending before the DRT?

Many litigants are surprised by the answer.